Current rates

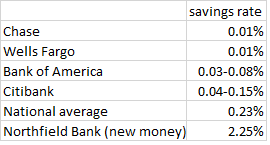

According to depositaccounts.com (from Lendingtree), here are current savings rates from the big banks:

With the national average at just 0.23%, you are likely not getting what you deserve. One offer currently paying the highest rate is from Northfield Bank in Staten Island, NY. They are paying 2.25% on new money up to $100,000 and there are no fees if you keep more than $2,500 at the bank. I'm not familiar with this bank so please do your due diligence. That said, over a full year, this account would pay $2250 in interest versus $10 from Chase or Wells Fargo. That's a good chunk of change that you shouldn't let fall through the cracks.

If you are looking for a larger institution, then a money market account from Capital One 360 pays 1.75% or Goldman Sach's Marcus pays 1.8%. Remember to stay under the FDIC insured limits of $250k per depositor, per FDIC insured institution. Also read the fine print to ensure that you aren't subject to account minimums or other fees.

Don't allow your money to sit idle, when it can be earning a risk free return!

Check your bank and let me know how much they are paying in the comments below.

Feature Image from GrokAI