On December 16, 2015, there was an update to this post.

Before reading this, please reference the up-to-date information at:

Qualified Charitable Distribution from IRAs Permanently Extended

For those of you at least 70½ years old, you are probably very aware of minimum required distributions (MRDs) that you are required to withdraw every year from your retirement account(s). What you may not know is that The Pension Protection Act of 2006 enabled IRA owners, age 70½ or over, to directly transfer up to $100,000 per year tax-free to an eligible charity. This option could be used for distributions from IRAs, regardless of whether the owners itemize their deductions. Moreover, the transfer counts as your required minimum distribution (RMD) but does not boost your adjusted gross income. As of this writing, however, Congress has not passed legislation permitting tax-free transfers from IRAs to charity.

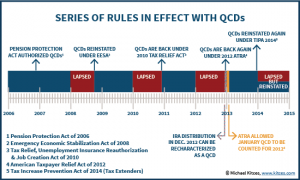

History of QCD Rule

Our complex tax code has meant inconsistent qualified charitable distribution (QCD) rules making it challenging for IRA owners to plan for their qualified charitable distributions. This year is no exception. Reference the below graphic to see how many times the rule has been reinstated and extended over the past eight years.

source: Michael Kitces, www.kitces.com

QCD Quick Summary

- Funds must be transferred directly by the IRA trustee to the eligible charity.

- Distributed amounts may be excluded from the IRA owner’s income.

- Amounts transferred to a charity from an IRA are counted in determining whether the owner has met the IRA’s required minimum distribution (RMD).

- Not all charities are eligible. Donor-advised funds and supporting organizations are not eligible recipients.

- Distributions from employer-sponsored retirement plans (e.g. SIMPLE IRA plans and simplified employee pension (SEP) plans) are not eligible.

What to Do in 2015?

Congress typically waits until mid-December to pass legislation permitting qualified charitable distributions from IRAs. In 2014, the IRS made the announcement on December 23rd giving IRA owners only 6 business days to complete their IRA distribution before January 1. In rare cases, like in 2013, Congress didn't approve the transfer until January 2013. If you want to donate your required minimum distribution to charity rather than taking it as a taxable withdrawal, you should wait until closer to the end of the year to take your RMD.

Ultimately, though, you may need to commit to making your charitable distributions first and hope that Congress extends QCD. The reason for the leap of faith is that you'll need to submit your RMD distribution request with ample time to process before year end or else you could be faced with a penalty of 50% of your RMD amount. In that light, be sure to make your 2015 required minimum distribution and let the tax treatment be secondary.

Have you taken your required minimum distribution yet for 2015? If you donate to charity, will you wait for a decision from Congress on QCD rules?

Feature Image from GrokAI