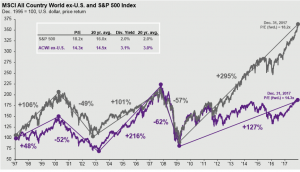

Here is the chart always universally referenced for the bull case for international stocks:

Runnymede favors US over International

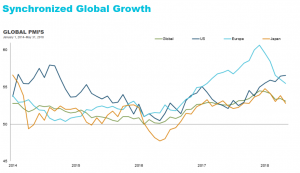

The way we saw it was that the US corporations would see big benefits from tax reform, not international corporations. Furthermore, the IMF said back in October that growth in Europe and Japan were expected to slow. As investors, we favor companies (and countries) with steady or accelerating growth over ones with decelerating growth. This has played out as we expected. Global growth has been good in 2018 but there has been a sharp slowdown in European and Japanese manufacturing as seen in the chart below.

US stocks leading the way

Given that US growth is the strongest, it is not surprising that US indices are leading the way this year. Technology stocks and small caps have reached new highs. Here are the results through June 14th.

Will US stocks continue to outperform international stocks forever? The answer is obviously no. At some point, international markets are bound to close the under-performance gap of the last 10 years. Reversion to the mean is almost inevitable. We just don't think the time is now.