It was brought to my attention that Christine Benz, Morningstar’s director of personal finance, predicts stocks will earn a meager 1.6% a year over the next decade. AQR's Portfolio Solutions Group says the expected real return of a U.S. 60/40 portfolio is just 1.4%, a fraction of its long-term average of nearly 5% (since 1900).

While the Runnymede investment team announced a financial hurricane alert on its April 6th client conference call and has advocated holding a cash position since the first quarter, I hadn't entertained the idea of low single-digit returns for an extended period. If this scenario played out, it would have significant implications for retirement planning and the operating budgets of many non-profit organizations.

Earnings Growth

First, I found this table at a Wealth of Common Sense. We always believe that earnings matter.

The good news is that there have been very few decades of negative returns for the S&P 500. The 1930s and 2000s stand out. Not surprisingly, we see that S&P 500 earnings growth was negative or in the single digits.

JP Morgan recently said that consensus earnings estimates for the S&P 500 are “overly pessimistic” for the first quarter and expects companies in the index to deliver earnings surprise of 4% to 5% on “better-than-feared margins.” For 2022, JP Morgan revised its S&P 500 earnings-per-share outlook from $235 down to $230, which implies a 10% earnings-per-share growth year-over-year. We will continue to track where S&P 500 EPS numbers are headed.

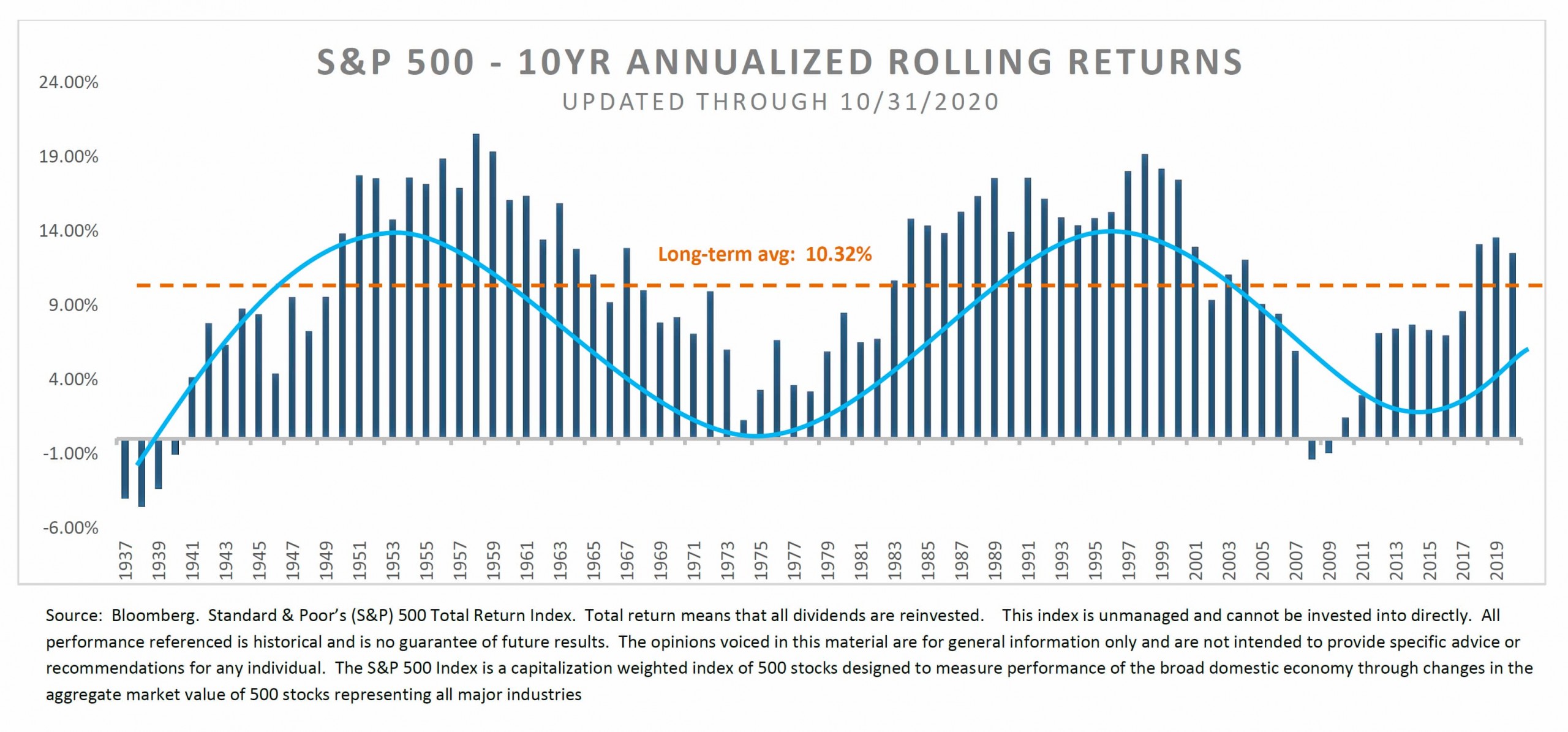

10-Year Returns

Second, the 10-year rolling returns of the S&P 500 paint a different picture. Since 2018, S&P 500 returns have been better than the long-term average of 10.3%.

Historically, once the long-term mean has been breached on the upside, annualized returns have remained elevated above the mean for an average of almost 18 years.

There have been very few times when 10-year annualized returns have fallen below 2%. Notably, the 1970s had low returns when inflation ran high.

The question remains, “How quickly can the Federal Reserve tame inflation?”

Predicting a decade's worth of equity returns is a very tough call. Looking at earnings growth and historical rolling 10-year returns, I am not convinced that long-term returns for the S&P 500 will be sub 2% going forward. Of course, the Federal Reserve may not be able to drop interest rates with inflation running hotter than it has in a long time. Any misstep by The Fed or its inability to add liquidity as it has in the past could put pressure on stock returns.

If there is a market correction, the risk to return profile for stocks will be more attractive. The key is to have cash that can be redeployed at better prices.

What expectations do you have for annual stock market returns? Are you assuming above or below 5%?

Feature Image from GrokAI