(Important note: since publishing this blog post in April 2014, cap rates have been lowered and spreads have gone up. In addition, the bonus rider has been reduced from 50% bonus to 25%. Both negatively affect potential returns of this product. This shouldn't be a surprise. As interest rates fall, you can expect returns to be smaller and smaller on index annuities.)

The annuity business has grown in popularity as investors, especially those nearing retirement, look for options to protect themselves from stock market volatility and give them a decent income stream in retirement. With over $200 billion in annual sales, the annuity industry is big business with lots of salesmen trying to persuade you to make a purchase.

Today I will dig deep into the best selling indexed annuity for the 4th quarter of 2013. Sales of indexed annuities, a fixed annuity that provides a minimum guaranteed rate of interest combined with an interest rate tied to movement of an index, increased to $39.3 billion in 2013, a 17% gain year over year. This is the biggest percentage increase of any form of annuity.

You will often hear that annuities are sold, not bought. This is exactly why I will go in depth into some of the most popular annuities because there is shockingly little information available about them. Most of the information comes from the companies that sell the annuities and they gloss over the fees, risks and downsides. More importantly, annuities have grown into extremely complex instruments which even the most season professional may have trouble deciphering. Indexed annuities, often the black sheep of retirement products, have a history of being so complex that they were a focal point of litigation and regulatory action in the 2000s. While the negative attention led to a change for the better among the carriers, indexed annuities are still complex and difficult to truly understand.

It is of the utmost importance to make an informed decision. I have dealt with too many clients that have come to me asking for help getting out of an annuity and I can't help after the fact. Stiff surrender penalties can't be avoided for many years after you sign on the dotted line.

A Perspective That You Can Trust

I am writing this blog from the perspective as a curious analyst. I am totally impartial as I am a fee only registered investment advisor. I hope to bring a unique perspective to this topic drawing on my years of experience analyzing companies as a research analyst. I've met with hundreds of company CEOs and CFOs, including Steve Jobs and Richard Branson, and I will use my analytical skills to break down these complex instruments into something easier to understand.

While many investment professionals hate annuities, I do not believe that they are all bad and some of them can make sense as a small part of your investment portfolio. Annuities should never, I repeat never, be the large majority of your portfolio because of their lack of liquidity which is one of their biggest drawbacks.

Issuer Review: Allianz SE and Allianz Life

It is important to look at the issuer of the annuity first because annuities are NOT a guaranteed investment of any sort. This is important to note so I will say it one more time. Annuities are NOT guaranteed. They are only backed by the ability of the issuing insurance company's ability to pay. Therefore if the issuer goes bankrupt, you are at risk of losing everything!

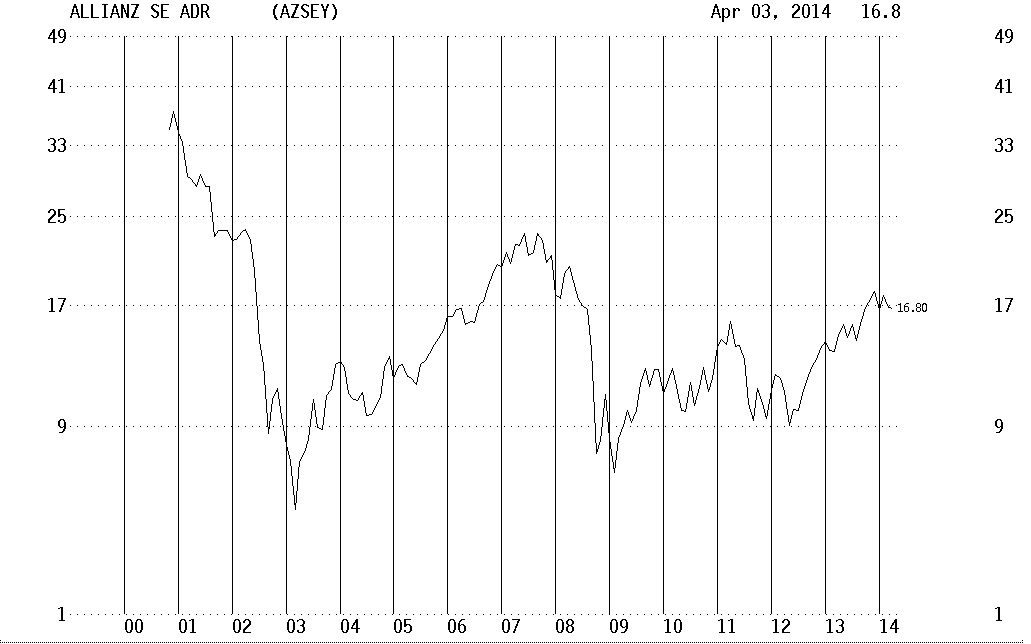

Allianz SE is a global financial services group headquartered in Munich, Germany.

It is the 2nd largest money manager in the world. Allianz in North America includes PIMCO and Allianz Global Investors. Here is a chart of Allianz SE:

It is the 2nd largest money manager in the world. Allianz in North America includes PIMCO and Allianz Global Investors. Here is a chart of Allianz SE:

Allianz Life receives solid ratings from all the leading rating agencies. S&P recently affirmed Allianz Life's AA Rating (very strong) with a stable outlook. This rating is the third highest out of 21 possible ratings. Moody's rates the company Aa3 with a stable outlook.

Allianz is the #1 seller of fixed annuities in the US. After a challenging year in 2012 when fixed annuities suffered a double digit decline, Allianz had a very strong 2012 with sales of fixed index annuities rising 11%. Sheryl Moore, CEO of annuity research firm Wink said she thinks Allianz's relative new “Allianz Preferred” program has boosted sales. She says, “The secret sauce is in that commission structure.” On the Allianz 360 Annuity, agents can earn 7.5% commission in year one in addition to commissions in following years.

Annuity Review: Allianz 360 Annuity with 360 Benefit Rider

Maximum age for initial purchase: 80

Minimum initial premium: $20,000; additional premium accepted through first 3 contract years

Rider fees: 1.05% for the 360 Benefit Rider

Website: www.allianzlife.com

Beware of Surrender Fees

Surrender charges and period for this annuity are the typical of most indexed annuities. Surrender fees go for 10 years and are 10% for the first 3 years. After the 1st contract year, you may withdraw 10% each year without surrender fees. However if you are under age 59.5, you are subject to a 10% IRS tax penalty as well as income taxes.

I believe surrender fees are one of the worst features of annuities. These are huge lockup fees and if you need the money, they sock it to you. This is why annuities should NEVER be a significant part of your investment portfolio because they are essentially illiquid for many years. Unless you are positive you will not need access to these funds, then annuities are NOT for you.

The Allianz pitch as per their brochure

Allianz highlights these points:

- Provides level payments for the rest of your life

- Provides lifetime income plus an opportunity for payment increases

- Principal protection

- Potential indexed interest (limited by caps, spreads and participation rates)

- Get a guaranteed minimum value

- 360 Benefit rider (additional cost) gives you an interest bonus of 25%

- Tax deferred growth

How will you likely be pitched this annuity?

This indexed annuity (also called an equity-indexed annuity, fixed-index annuity or hybrid annuity) will likely be packaged around two main components:

1. Principle protection with upside potential from their attractive index choices

2. 25% interest bonus from the 360 Benefit Rider

I'm quite certain that this annuity is being pitched too aggressively in terms of expected return as Allianz saw a surge in sales at the end of last year. Last year was a big year for the monthly sum crediting option which would have given you 10%+ “return” for 2013 but this I assure you is the exception, not the norm. Over the long term, this annuity will generate returns of 2-4%. Anything more is a pipe dream.

The 50% interest bonus from the 360 Benefit Rider sounds appealing. Many agents will give an example of: if the index goes up 6% in a year with the 50% bonus, you get credited 9%. Great sales pitch but not the reality. With true returns of 2-4% over time, your 50% bonus will be between 1-2% and once you subtract the 1.05% annual fee, it is even less and perhaps zero.

(Note: This interest bonus has been reduced to 25% as of June 2014. This makes the 1.05% cost even more suspect.)

Given the shrinking cap rates in 2014/5, you will likely be sold on the Barclays Dynamic Index which shows the best hypothetical returns. Just note that spreads have been rising dramatically from 2.9% in 2014 to 4.15% as of February 2015. Therefore don't be surprised to have a spread of 5% in 2016 which means lower returns for you!

I have heard that some agents are indicating potential returns of 8%+. Let me say that this is an incredible sales pitch. Who doesn't want 8% returns with no downside risk? There is one other person that promised those returns and his name is Bernie Madoff. Please do not trust anyone that promises even 6% returns with no downside risk. It is too good to be true. Trust your instincts and run if any agent is selling you that dream.

Here is a quote from a National Sales Director of annuities that I'm connected with on LinkedIn. “A big concern I have is not the product, but that some of advisors and agents I've spoken with who sell it – and possibly not properly trained – seem to spend too much time on the now 25 year historical illustration view instead of the guarantee and ten year illustration pages. Many do not realize that bringing in 1989 into play (the then Lehman Bond Aggregate [now Barclay's] was 17.95% that year, and the S&P was over 31%) and showing the illustration to clients might create some overly hopeful growth.”

Let's dig into this annuity so you have a better understanding of the nuts and bolts…

Interest Crediting Options

It is important to understand that you are not investing in the underlying securities of any index. With index annuities, you are not making investment choices like a variable annuity. Your interest crediting options are mathematical formulas that the insurance company is using to attract you into buying xyz annuity. The insurance company invests your money in whatever they choose (likely diversified, conservative investments). They just have to earn a return higher than their mathematical formula (or interest crediting option) so they can pay you, their sales force, marketing, operations, etc. This is why index annuities will only generate low single digit returns.

For the Allianz 360 Annuity, you may select from 6 different interest crediting options: the Fixed interest allocation and Indexed interest allocations (S&P 500, Nasdaq 100, Russell 2000, Barclays US Dynamic Balanced Index and a blended index). To make it a bit more complex, you have three different crediting methods: monthly sum crediting, annual point-to-point crediting and monthly average crediting. So let's dig a bit deeper into your choices.

As of April 1, 2014, the Fixed interest allocation is currently paying 1.30% (As of Feb 2015, 1.1%). I'm not sure why anyone would want this option. You can buy a 5-year Treasury Note and earn 1.79%. You can beat the fixed account on your own.

So onto the Indexed interest options. Many salespeople may sell you on high returns but none of these options will deliver much more than 3% returns. If someone is promising higher returns then you need to find a more honest agent. Whatever option and crediting method you choose, you will likely make around 1-3% over the long term. I will illustrate this for you.

Let's first look at the monthly sum crediting method which looks at the index return with a cap (currently 1.7% for Nasdaq 100 and S&P 500 and 2.3% for Russell 2000 as of April 1, 2014).

NOTE: These rates have already declined to 1.5% for Nasdaq and S&P and 2.1% for Russell 2000 as of May 6th, 2014! (Note as of 2/3/15, caps have fallen again. 1.3% for Nasdaq and S&P and 1.9% for the Russell 2000.)

This cap can be changed from year to year but will never be less than 0.5%. There is no cap on negative months. For example, if the S&P went up 6% in January, you'd be credited with 1.3%. However if the S&P went down 7%, you'd be credited with -7% for that month. At the end of the year, the totals are added up and that is your return for the year. If it is negative, you don't lose anything. Here is an example for 2012:

| Date | S&P 500 | Monthly % chg | Allianz 360 |

| Jan-12 | 1312.41 | 4.36 | 1.30 |

| Feb-12 | 1365.68 | 4.06 | 1.30 |

| Mar-12 | 1408.47 | 3.13 | 1.30 |

| Apr-12 | 1397.91 | -0.75 | -0.75 |

| May-12 | 1310.33 | -6.27 | -6.27 |

| Jun-12 | 1362.16 | 3.96 | 1.30 |

| Jul-12 | 1379.32 | 1.26 | 1.26 |

| Aug-12 | 1406.58 | 1.98 | 1.30 |

| Sep-12 | 1440.67 | 2.42 | 1.30 |

| Oct-12 | 1412.16 | -1.98 | -1.98 |

| Nov-12 | 1416.18 | 0.28 | 0.28 |

| Dec-12 | 1426.19 | 0.71 | 0.71 |

| 13.40 | 1.06 |

In 2012, if you actually invested in the S&P 500 by purchasing an ETF like SPY, you would have been up 16% thanks to price appreciation and dividends. The S&P 500 without dividends was up 13.4%. In the Allianz 360 Annuity, if you selected monthly sum crediting, you would be credited with a paltry gain of just 1.06%. If you selected the annual point-to-point crediting option, you would receive 1.75% (April 2014 cap was 3%).

(Note January 2015 cap rates have fallen to 2.25%) (New note: cap rates fell again in February to just 1.75%!)

Let's take a look at how the Allianz 360 annuity would fare over the last 10 years. Note that these are hypothetical returns because the Allianz 360 annuity launched in the summer of 2011.

| Allianz 360 | |||

| S&P 500 ex dividend | monthly sum | point to point | |

| 2013 | 29.6 | 8.2 | 1.75 |

| 2012 | 13.4 | 1.1 | 1.75 |

| 2011 | 0.0 | 0 | 0 |

| 2010 | 12.8 | 0 | 1.75 |

| 2009 | 23.5 | 0 | 1.75 |

| 2008 | -38.5 | 0 | 0 |

| 2007 | 3.5 | 0 | 1.75 |

| 2006 | 13.6 | 7.6 | 1.75 |

| 2005 | 3.0 | 0 | 1.75 |

| 2004 | 9.0 | 3.4 | 1.75 |

| average | 2.0 | 1.4 |

The monthly sum method performed slightly better than the annual point-to-point option on the S&P but both returned around 2%. As you can see, the monthly sum method produced a couple of big years (2006 and 2013) but were offset by many big fat zeros. If you would like to see the numbers in more detail, just shoot me an email via our secure form and I'd be glad to share the numbers with you.

The Barclays US Dynamic Balance Index is another interesting option. It has been very good over the past 5 years. Of course that period was a great time to be in equities and not this index. If you go back 5 more years, it is no surprise that this choice also yields a return of 3%+. Here are the numbers using the current spread of 2.9%

(Note this spread has jumped to 3.4% as of May 6th, 2014!) (Note this is 3.65% as of Jan 2015) (New Note, the spread jumped to 4.15% as of February!)

The spread is subtracted from the yearly percent change. Note that the maximum annual spread is 12%! Your return for any given year will never be lower than zero.

| Date |

US Dynamic Balance Index TR |

% change | Allianz 360 |

| Dec-03 | 340.2463 | ||

| Dec-04 | 357.3282 | 5.0 | 0.9 |

| Dec-05 | 361.2923 | 1.1 | 0.0 |

| Dec-06 | 401.2476 | 11.1 | 7.0 |

| Dec-07 | 417.5862 | 4.1 | 0.0 |

| Dec-08 | 410.8596 | -1.6 | 0.0 |

| Dec-09 | 451.9316 | 10.0 | 5.9 |

| Dec-10 | 493.1369 | 9.1 | 5.0 |

| Dec-11 | 513.618 | 4.2 | 0.1 |

| Dec-12 | 545.1212 | 6.1 | 2.7 |

| Dec-13 | 603.8816 | 10.8 | 6.7 |

| 5 year | 4.1 | ||

| 10 year | 2.8 |

2013 was a very compelling year for the monthly sum option as the S&P, Nasdaq and Russell would have posted over good gains for the Allianz 360 owner. However you shouldn't expect this type of return over an extended period as 2013 was an exception, not the norm. Looking back 5-10 years with the stellar 2013 included, all of the choices yield between 1-3% annual returns. If you are satisfied with these types of returns then it is fine. I just don't want you to expect more because you will surely be disappointed.

If you have additional questions about these options, please submit a question using our secure form. We will answer your questions within 24 hours via email. No strings attached, just a little free help to point you in the right direction.

Who should buy this product?

In summary, the Allianz 360 Annuity is something to consider for someone that doesn't want to worry about market volatility, won't need access to their money for at least 10 years and is happy with low single-digit returns of 1-3%. The annuity can make sense for an extremely conservative investor who is looking for guaranteed income with no market risk. If you are happy with low investment returns and a guaranteed income stream, then this product may be acceptable for you. Be sure to evaluate how it fits into your entire investment strategy and how it will help you reach your financial goals.

In the end, all of the interest crediting options will pay roughly 1-3% over a full market cycle. If this gets too far out of line, Allianz will adjust the caps (to as low as 0.5%/month) and spreads (12% max) because they can't afford to pay more.

(Note that Allianz has already lowered caps and raised the spreads just one month after I wrote this blog post and then have fallen dramatically in 2015. You shouldn't be surprised by this as interest rates fall, insurance companies can't pay much on index annuities.)

Don't buy into any sales pitch that is promising rates of return of 8-12% or more. It just isn't possible to generate 10% returns with no downside risk. If anyone promises you even 5%+ returns for this annuity, don't just walk away, run for the door and find a new advisor. For Allianz to pay 5% on this annuity, they would have to earn 9%+ on their own investment portfolio so they could pay you as well as their salespeople, marketing and overhead, not to mention to earn a profit themselves. Commissions are very lucrative for agents selling the Allianz 360 so be sure that you make the right decision for you, not for their benefit.

Thanks for sticking with me on this incredibly long blog post. I learned a lot in my research process and I hope you are able to make a more informed investment decision because of it. Please don't let your agent pressure you into a sale before you have made an informed decision. Since annuities lock you into a long-term contract with stiff surrender fees, please be sure to take your time to make the best possible decision for you and your family.

Have questions about this Annuity?

If you're considering this annuity and have additional questions, feel free to reach out. You can contact us via our secure contact form. We will answer your questions within 24 hours via email. No strings attached, just a little free help to point you in the right direction.

If you have questions about this annuity, please share them in the comments section below or visit our secure page to submit a question.

Feature image from GrokAI