An Emphatic No!

Simply put, there is no way that index annuities will ever produce stock market returns over the life of the product, and they should be thought of as a fixed income alternative, not a stock alternative. When they throw in index choices like the S&P 500, this just makes potential buyers have unrealistic expectations.

So how can I say these products will never produce equity-like returns? It's simple. Just look at how the insurance company is investing the underlying assets. Remember that index annuities don't own any underlying assets (stocks or bonds) like a variable annuity. It is purely an insurance contract and the insurance company invests as they please.

Here's Why. How does the insurance company invest?

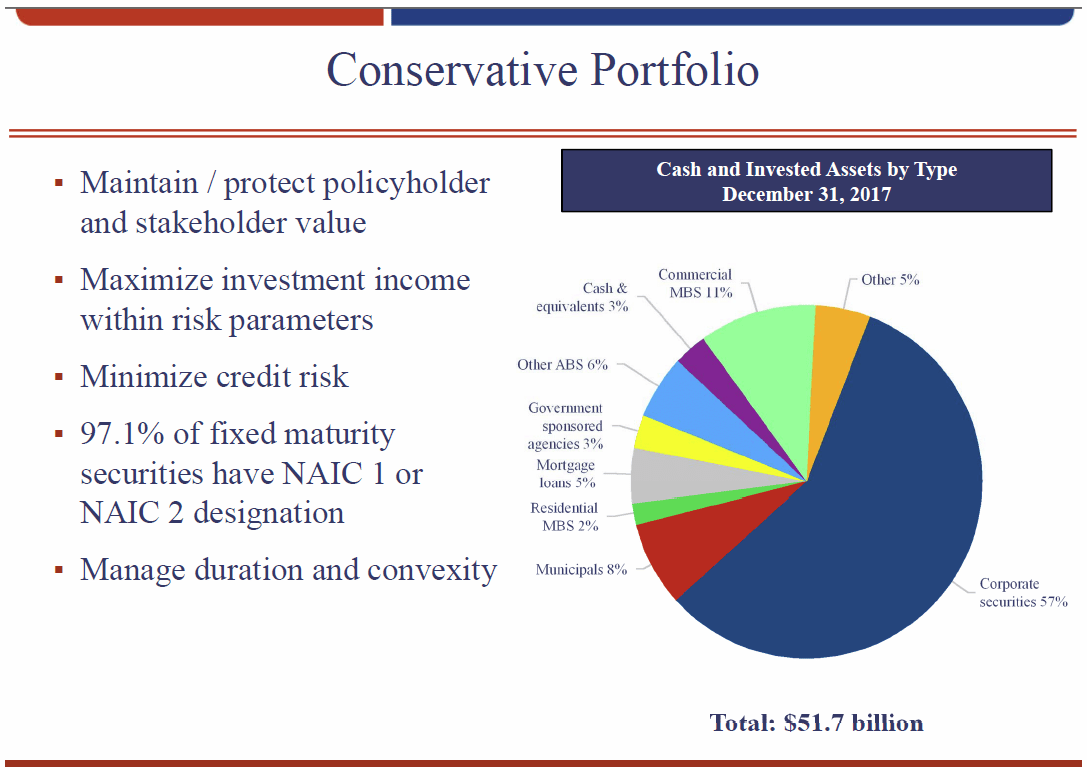

Luckily one of the top 3 index annuity providers is a public company so they show exactly how they invest. As of December 31, 2017, 96% of their products sold are fixed index annuities and they have been a top 3 producer by annual sales for 16 out of the last 17 years. Here is how they invest their money:

It is not surprising that their investment portfolio is extremely conservative since their products have no downside risk. If you look at the breakdown, the entire pie is fixed income/bonds with NO stock market exposure. After they pay their agents, staff, rent, executives, marketing and more, they still earn a profit for shareholders, but that comes at the policyholders' expense.

In Conclusion

This top insurance company invests all of its investment portfolio in fixed income assets. After paying out all their expenses and earning a healthy profit margin on top of that, then they can pay out policy holders a low return. It seems clear to me that most people will be better off investing themselves directly in fixed income assets and cutting out the middle man.

Buyers of annuities will be okay if they see these products for what they are: longevity insurance. They can be used for a small part of an investment portfolio for their safety where they can provide a guaranteed income for life. But never expect anything close to stock market returns! This type of annuity works best for those in great health and a family history of longevity. Because if you live into your 90s, you will likely do okay thanks to the guaranteed income rider; however for the majority of policy holders, they would be better off investing themselves in a conservative portfolio of stocks and bonds.

If you own an index annuity, has it met your expectations?.

Feature Image from GrokAI