The annuity business has grown in popularity as investors, especially those nearing retirement, look for options that protect them from stock market volatility and provide a decent income stream in retirement. With over $200 billion in annual sales, the annuity industry is big business with lots of salespeople trying to persuade you to make a purchase.

Today, I will dig deep into the Allianz Index Advantage Income Annuity, one of the insurance industry's newest innovations. Registered index-linked annuities, RILAs also known as buffer annuities, appeal to investors who are risk averse but also need growth because they offer some downside protection in exchange for a cap on a stock index's upside performance. If it sounds attractive, you're not alone. Sales of RILAs rose 38% to $4.9 billion in the first quarter of 2020.

You often hear that annuities are sold, not bought. And you're likely here trying to do your research and due diligence before purchasing. This is exactly why I write reviews on some of the most popular annuities. Frankly, there is shockingly little information available about them. Most of the information published comes from the companies that issue and sell the annuities, and I find that they gloss over the fees, risks, and downsides. More importantly, annuities have grown into extremely complex instruments which even the most seasoned professional may have trouble deciphering. Indexed annuities, often the black sheep of retirement products, have a history of being so complex that they were a focal point of litigation and regulatory action in the 2000s. While the negative attention led to a change for the better among carriers, indexed annuities remain complex and difficult to truly understand.

The key to buying any insurance product is to understand what it does and select the product that best fits your needs. I have personally dealt with too many clients who have come to me asking for help getting out of an annuity that turned out not to be a good fit. Unfortunately, I can’t help after the fact. Stiff surrender penalties can’t be avoided after clients sign on the dotted line. Hopefully, I can help you make the best decision ahead of buyer's remorse.

Perspective That You Can Trust

I write this blog from the perspective of a curious analyst who looks at many investments and strategies. As a fee-only financial advisor, I tend to be more objective than a commissioned salesperson. I hope to bring a unique perspective to this topic drawing on my years of experience analyzing companies as a research analyst. I’ve met with hundreds of company CEOs and CFOs, including Steve Jobs and Richard Branson, and I will use my analytical skills to break down these complex instruments into something easier to understand.

While many investment professionals hate annuities, I do not believe that they are all bad and certain products can make sense as part of your investment portfolio. Annuities should never, I repeat never, be the large majority of your portfolio because of their lack of liquidity, one of their biggest drawbacks.

Issuer Review: Allianz SE and Allianz Life

It is important to look at the issuer of the annuity first because annuities are NOT a guaranteed investment of any sort. This is important to note so I will say it one more time. Annuities are NOT guaranteed. They are only backed by the ability of the issuing insurance company’s ability to pay.

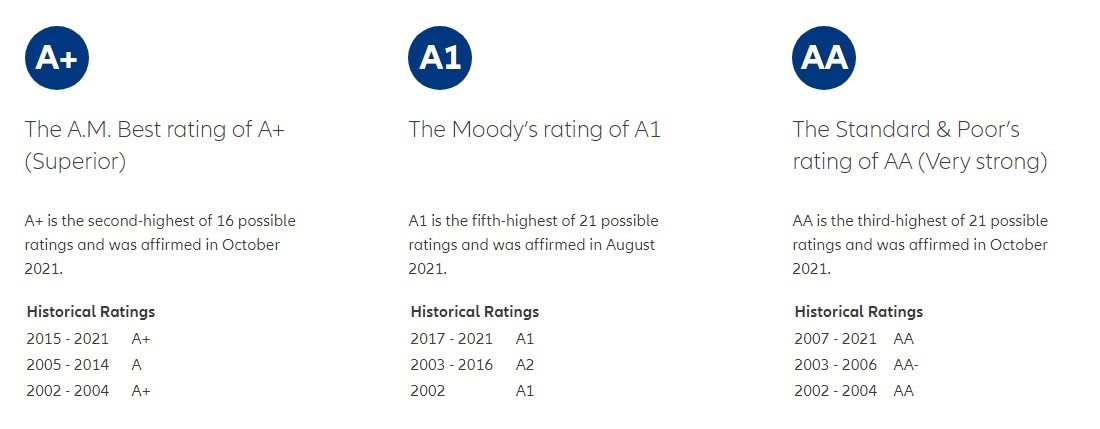

Allianz SE is a global financial services group headquartered in Munich, Germany.

It is the 5th largest money manager in the world. Allianz in North America includes PIMCO and Allianz Global Investors.

Allianz Life receives solid ratings from all the leading rating agencies as of 2021.

Annuity Review: Allianz Index Advantage Annuity

Maximum age for initial purchase: 80 (75 if you select the Maximum Anniversary Value Death Benefit)

Minimum initial premium: $5,000

Website: www.allianzlife.com

Fee: 1.95 percent (1.25% annual product fee plus 0.7% Income Benefit Rider fee); 0.2% for optional Maximum Anniversary Value Death Benefit

NOTE: Runnymede offers a commission-free version of The Allianz Index Advantage Income ADV Variable Annuity that carries a fee of 1.45% (0.75% annual fee + 0.7% Income Benefit Rider). This cost savings will increase your return. Schedule a call for details.

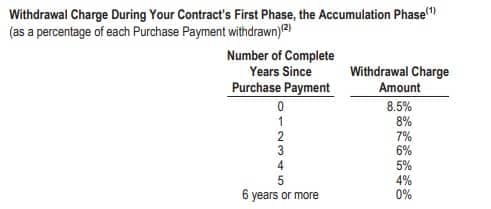

Beware of Surrender Fees

Surrender charges and period for this annuity are typical of most annuities. The contract includes a 7-year withdrawal charge schedule.

After the 1st contract year, you may withdraw 10% each year without surrender fees. However, if you are under age 59.5, you will be subject to a 10% IRS tax penalty as well as income taxes.

I believe surrender fees are one of the worst features of annuities. These are huge lockup fees and if you need the money, they sock it to you. This is why annuities should NEVER be a significant part of your investment portfolio because they are essentially illiquid for many years.

If there is any chance that you will need the cash you're considering putting into this annuity, stop reading now! Only proceed if you are positive that you will not need to access these funds over the next seven years.

A quick note: My firm has access to many commission-free versions of annuity products from Allianz and other companies. In the case of the Allianz Index Advantage Income ADV Variable Annuity, the commission-free version is not only available to you at a lower cost but has NO surrender fees. This is a huge benefit along with cost savings. If this interests you, we should talk.

The Allianz pitch as per their prospectus

Allianz highlights these points:

- Buffered downside protection

- Potential uncapped growth

- Income stream for life

How will you likely be pitched this annuity?

This indexed variable annuity (also called a buffered annuity) will likely be packaged around three main components:

1. Uncapped potential growth of the S&P 500; or high caps on other indexes;

2. Buffered protection of 20% for a 3 or 6 year period; or 10% buffer on 1 year periods.

3. Lifetime income payments with potential for increasing payments over time.

This product can make sense for someone who is looking for growth but also concerned about downside risk and is looking for a way to guarantee an income stream for life. It can provide uncapped upside potential in the S&P and also gives 20% buffered protection for 3 year periods. I will go into this in more detail in a bit.

Let's dig into this annuity so you have a better understanding of its features and options.

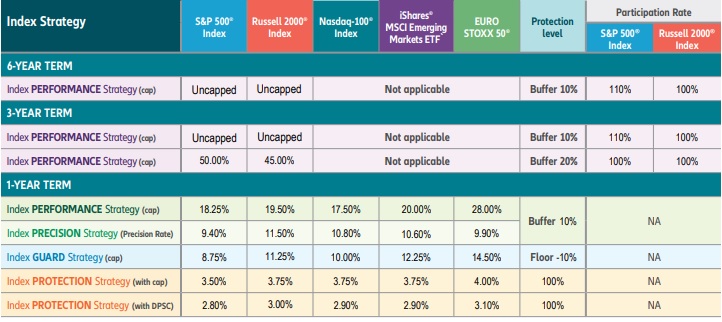

Interest Crediting Options

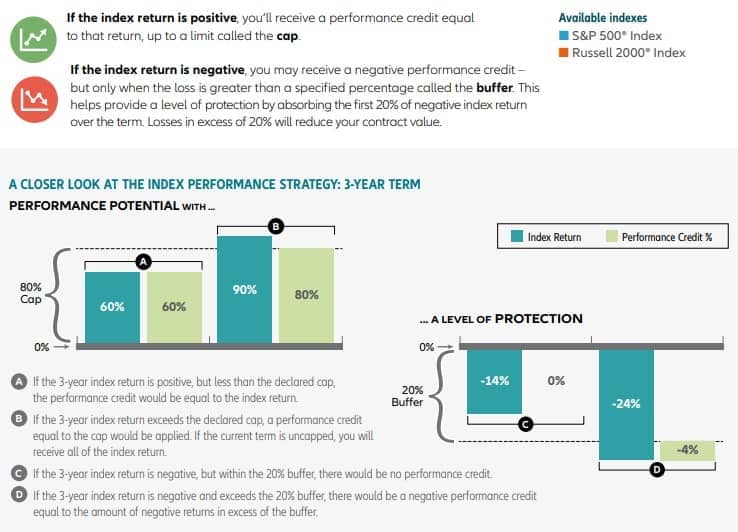

One intriguing option for this product is the 3-year or 6-year term strategy. This offers 10% downside protection and either uncapped growth of the S&P 500 or the Russell 2000. Another option is for capped growth of 50% for the S&P 500 or 45% for the Russell 2000 with a 20% buffer.

The downside protection or buffer is calculated every 3 years. For example, at the end of 3-years, if the S&P 500 has gained 50% in price, your account value has increased by 50% minus the annual fee. However, if the index dropped by 10% over that period, you would lose nothing as it is within the 20% buffer. If the S&P loses 25% in the 3 years, then you would have a loss of just 5% (25% – 20% = 5%).

The rest of the strategies are one-year term strategies. The buffer is 10% for all the one-year strategies.

In the one-year term structure, you have more index choices: the Nasdaq 100, iShares Emerging markets, and the Euro Stoxx-50. Here is the current cap structure (11/2/21-12/6/21):

If you take the performance strategy in a 1-year term, your cap on the S&P 500 is 18.25% and your buffer is 10%. This gives some downside protection and a very sizable cap as the S&P 500 isn't typically up more than 18.25% in one year.

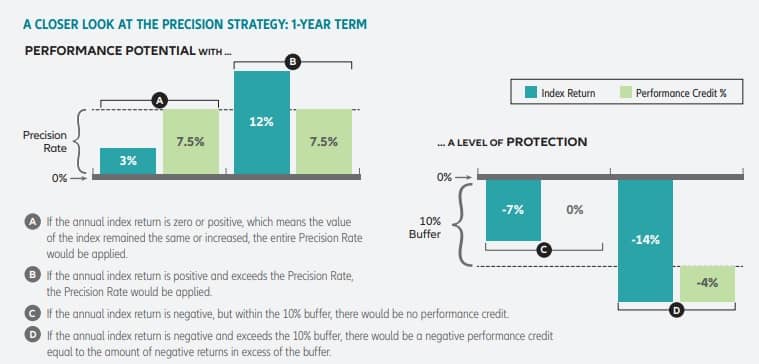

The Precision strategy is also known as a trigger strategy. If the return in the index is zero or positive, you earn “Precision rate.” Referencing the rate table above, if the S&P returns 1% at the end of your contract year, you would earn 9.4% in your contract for that year. Your downside is buffered by 10%.

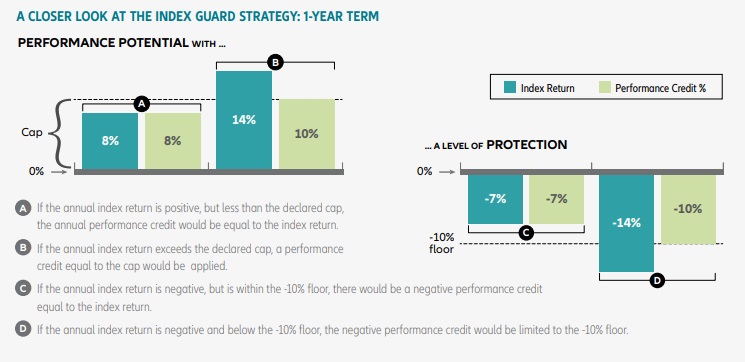

The Index Guard strategy offers downside protection in a different way. You are responsible for up to a 10% loss in the index but you can't lose any more than that. However, your upside is also capped at lower levels as you can see in the table above. For the S&P 500, you are capped at 8.75%.

The Protection strategy gives you 100% downside protection. This is essentially a bond alternative offering 2.8-3.5% caps with 100% downside protection.

Guaranteed Lifetime Income

With this annuity, you have to take the Income rider which cost 0.7% annually (if you do not need income, you should look at the Allianz Index Advantage annuity instead). Even if you contract value goes to zero, you still get paid with this income rider so it obviously pays more if you live a long life.

Keep in mind that you have to wait at least 3 years until you can start taking your income payments. Furthermore, the longer you wait, the higher your income payment (similar to a social security calculation). Each year that you wait, you get an additional annual increase percentage based on your age at purchase. For example, if you purchase before age 55, you get a 0.25% per year that you wait vs if you are age 80, you get a 0.55% per year increase.

You also have two choices for your income payments as you can either select level payments or increasing income. With level payments, your withdrawal percentage is 80bps higher and the payment stays the same for the rest of your life. With increasing payments, your withdrawal percentage is slightly lower initially but you have the chance to increase your payment over time. During the income period of the annuity, you have to select one of the Protection strategies so your income can rise by up to 3.5% annually given current rates. This is pretty attractive and can help offset rising inflation over time.

Here is a link to the lifetime income percentage charts.

You can also use the Allianz income calculator to see how much retirement income you could potentially create.

Income Multiplier Benefit

The Income rider comes with an Income Multiplier Benefit for no additional cost. After a required waiting period (5 contract years), this can increase your income to help pay for care if you should need it. Currently, this multiplier benefit would pay double the income if you meet a certain level of needed care.

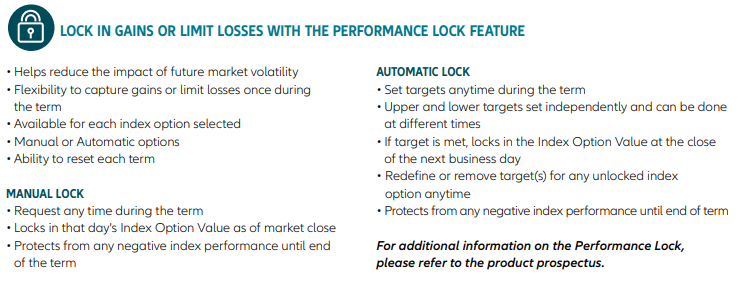

Performance Lock

One additional feature of this annuity is that it has the ability to lock in gains. This can be beneficial in a strong year like 2021 where you can ensure that you don't give back gains. This can be set up to be done automatically or manually.

Once you lock for the year/term, you lock in the index value as of the market close. If you are in a multi-year strategy, you can lock performance and then start a new term in the following year, you don't have to wait for the term to end.

Here are the details.

Who should buy this product?

In summary, the Allianz Index Advantage Income Variable Annuity is a product to consider if you are looking to grow your assets but also looking for some downside protection. It also provides a valuable lifetime income stream which can work as part of a financial plan. As detailed above, there are choices to make like selecting the index and the term, each has different upside caps and downside buffers. If you need help understanding the product's features and whether it fits well into your financial plan, schedule a call with me.

Runnymede offers a commission-free version of this product that carries a fee of 1.45%. Most agents offer this product with an annual fee of 1.95%.

Purchasing the same product with a lower fee means more money for you over the life of the contract. On a $250,000 investment, you could save at least $1,250 per year. Schedule a call for information.

Have questions about this Annuity?

If you found this article helpful, please leave a comment below. If you're considering this annuity, have additional questions, or want to buy this annuity at a discount, I'm happy to take the conversation off-line.

You can email me (Chris) directly at cwang@runnymede.com or via our secure contact form. We will answer your questions within 24 hours via email. No strings attached.

I want you to make the best decision with your money and am happy to point you in the right direction.

Feature image from GrokAI