The bonus is on the Protected Income Value, not your Principal

This is the most important thing to understand. The 30 percent bonus gives your Protected Income Value (PIV) a boost from day one. However, this doesn't increase your account value. If you don't know the difference between the two numbers then I implore you to do so if you are considering a purchase.

The simple way to think about this is that your account value is your walk away money. If you need your cash next week or next year, your account value can be accessed anytime (minus penalties during the surrender period). So if you put in $100k, this is roughly the amount that will be available.

The PIV gets a boost of 30 percent. The PIV can't be withdrawn in a lump sum like the account value. The PIV is only there to calculate your income payments when you decide to take your lifetime income payments.

Let's take a look at an example.

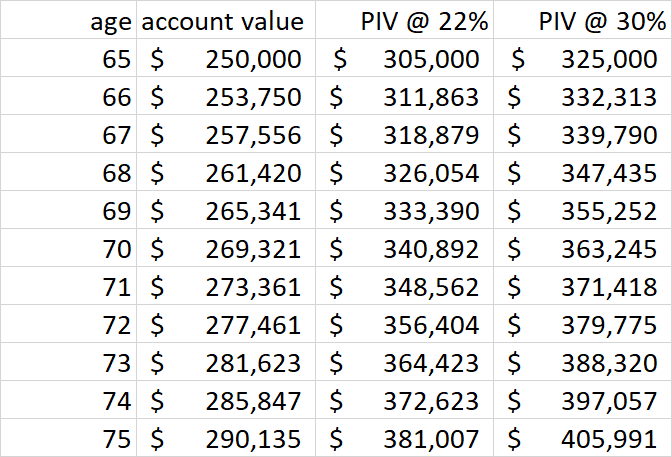

In this illustration, let's say Joan decides to put in $250k as her initial premium at age 65. For simplicity, I'm using straight line returns of 1.5% every year, which gets increased by 50% to 2.25% in the PIV. I also show you the difference between a 22% vs a 30% premium bonus.

As you can see, the difference between the account value and PIV is extremely large after 10 years. The account value has increased to $290k, while the PIV is up to almost $406k.

At 75, Joan decides to start taking income payments and her withdrawal rate is 5.5% as a single person. She can take $22,330 ($405,991 x 5.5%) vs $20,955 if the initial bonus was 22%. The extra bonus is essentially giving her an extra $1374 annually, which is a nice chunk of change. While this seems great, remember that income payments come out of your principal first and draw down your account value. So you really benefit when you are drawing income when your account value is zero, but that doesn't happen until Joan is at least 88 in this example. Given that life expectancy is currently 79, most of us won't see that day. In the end index annuities should be considered longevity insurance so it fits best for those in great health and a family history of longevity.

Conclusion

If you think that the Allianz 222 annuity is a good fit for your financial situation, then it is a great time to purchase. The extra bonus will mean higher income payments over time which is a good thing. Just be sure that you won't need the money before 10 years because if you take money before that time, then you will lose the bonus in proportion to how much money is withdrawn. Please read this footnote from the Allianz 222 website: To receive the PIV, including the bonus, the contract must be held for at least 10 contract years, and then lifetime income withdrawals must be taken. You will not receive the bonuses if the contract is fully surrendered or if traditional annuitization payments are taken. If it is partially surrendered the PIV will be reduced proportionally, which could result in a partial loss of bonuses.

I recommend limiting all annuity products to less than 25% of your investable assets due to the lack of liquidity. Index annuities like the Allianz 222 work best for those people who are in good health and have a family history of longevity. Remember that when you begin taking income payments, those come out of your principal first. If you live until you are into your 90 or 100s, then this product starts paying off and acts as longevity insurance; but if you aren't in good health, then this product probably isn't a good choice.

Feature image from GrokAI