The annuity business has grown in popularity as investors, especially those nearing retirement, look for options to protect themselves from stock market volatility and give them a decent income stream in retirement. With over $200 billion in annual sales, the annuity industry is big business with lots of salesmen trying to persuade you to make a purchase.

Today I will dig deep into an indexed annuity which has been booming in popularity in recent years. Sales of indexed annuities, a fixed annuity that provides a minimum guaranteed rate of interest combined with an interest rate tied to the movement of an index, increased to $39.3 billion in 2013, a 17% gain year over year. This is the biggest percentage increase of any form of annuity.

You will often hear that annuities are sold, not bought. This is exactly why I will go in depth into some of the most popular annuities because there is shockingly little information available about them. Most of the information comes from the companies that sell the annuities and they gloss over the fees, risks and downsides. More importantly, annuities have grown into extremely complex instruments which even the most seasoned professional may have trouble deciphering. Indexed annuities, often the black sheep of retirement products, have a history of being so complex that they were a focal point of litigation and regulatory action in the 2000s. While the negative attention led to a change for the better among the carriers, indexed annuities are still complex and difficult to truly understand for the average investor.

It is of the utmost importance to make an informed decision. I have dealt with too many clients that have come to me asking for help getting out of an annuity and I can’t help after the fact. Stiff surrender penalties can’t be avoided for many years after you sign on the dotted line.

A Perspective That You Can Trust

I am writing this blog from the perspective of a curious analyst. I am totally impartial as I am a fee-only registered investment advisor. I hope to bring a unique perspective to this topic drawing on my years of experience analyzing companies as a research analyst. I’ve met with hundreds of company CEOs and CFOs, including Steve Jobs and Richard Branson, and I will use my analytical skills to break down these complex instruments into something easier to understand.

While many investment professionals hate annuities, I do not believe that they are all bad and some of them can make sense as a small part of your investment portfolio. Annuities should never, I repeat never, be the large majority of your portfolio because of their lack of liquidity which is one of their biggest drawbacks.

Issuer Review: Security Benefit

It is important to look at the issuer of the annuity first because annuities are NOT a guaranteed investment by the FDIC, SIPC or any other federal agency. They are only backed by the ability of the issuing insurance company’s ability to pay.

Security Benefit is a turnaround story. The company was on death's door during the Financial Crisis of 2008-9, but today is coming off its best year ever. Sales at Security Benefit have grown from about $1 billion in 2010 to a record $7 billion in 2013. It created several fixed index annuities that provide steady income for life and possible upside if the stock market is positive. Today, Security Benefit has two of the top selling annuity products in this space nationwide and has a 12.3% market share, behind just Allianz, in indexed annuity sales.

Security Benefit's credit rating fell to non-investment grade status in 2009. This rating has recovered in recent years. In May 2012, Standard & Poor's upgraded Security Benefit to A- from BBB+. S&P stated that the outlook on SBLIC is stable, but it is unlikely to raise the rating during the next two years.

S&P warned, “We could lower the rating if margins on the new business being written compress due to assumptions on the product deviating from pricing estimates. In particular, we will be focusing on the lapsation utilization and the market dynamics that affect the GMWB rider. We would view adverse performance quite negatively as the company already possesses a narrow earnings profile. We could also lower the rating if the company doesn't maintain redundancy at the “AA level of capital.”

In August 2013, A.M. Best affirmed its rating of B++ (Good) and issuer credit ratings of “bbb+.” A.M. Best warned that “factors that could lead to negative rating actions are Security Benefit Life having an increase in its exposure to higher risk assets to support spread margin, a decrease in its risk-adjusted capitalization due to operating results and unfavorable investment performance, as well as continued accelerated growth in its fixed-indexed annuity liabilities.”

Annuity Review: Security Benefit Secure Income Annuity

Product launched: 2011

Maximum age for initial purchase: 80

Minimum initial premium: $25,000; Subsequent: $1,000

Maximum Purchase Amount: $1,000,000

Rider fees: Income Rider (GLWB): 0.95% per year, may increase to no more than 1.50%. The fees are guaranteed for the length of the Stacking Roll Up Term.

Website: www.securitybenefit.com

Beware of Surrender Fees

The surrender charges and periods for this annuity are very distressing like most index annuities. The double-digit fees for the first 3 years are tough to stomach if you need the money in an emergency. This is essentially illiquid for those years unless you just want to give your money away to Security Benefit. Here is the surrender charge schedule for most states.

I believe surrender fees are one of the worst features of annuities. These are huge lockup fees and if you need the money, they sock it to you. This is why annuities should NEVER be a significant part of your investment portfolio because they are essentially illiquid for many years. Unless you are positive you will not need access to these funds, then annuities are NOT for you.

The good news is that the contract owners may access funds under several circumstances. After the 1st contract year, you may withdraw 10% each year without surrender fees. However, if you are under age 59.5, you are subject to a 10% IRS tax penalty as well as ordinary income taxes. The contract does include a Nursing Home waiver and a Terminal Illness waiver which allows penalty free withdrawals (Not approved in all states and other state variations may apply).

The Standard Benefit TVA pitch as per theirbrochure

Standard Benefit highlights these points:

- 8% bonus (less in some states)

- 10% free annual withdrawals (after first full contract year)

- Guaranteed minimum interest rate

- Multiple interest-crediting options

- Nursing home waiver and terminal illness waiver (not available in all states)

- optional GLWB rider with 7% annual roll-up; home healthcare doubler

How will you likely be pitched this annuity?

This indexed annuity (also called an equity-indexed annuity, fixed-index annuity or hybrid annuity) will likely be packaged around two main components:

- Principle protection with upside potential using a capped S&P 500 option

- Guaranteed income for life with the GLWB rider

Unlike theTotal Value Annuity, the interest crediting options are a bit simpler with the Secure Income annuity. You have two different capped interest crediting options that are centered on the S&P 500. Even though you are likely familiar with the S&P 500 index, it is important to understand that if you purchase this annuity, you do not own the underlying assets of a mutual fund or stocks that are in the S&P 500 index. This is a mathematical formula that uses the S&P 500 to calculate your interest and nothing more.

The GLWB rider offers an attractive 7% roll-up rate but it is important to understand that this is not your rate of return. The 7% roll-up rate will increase your benefit base but you can't access this sum if you needed to make a withdrawal from your account value – the benefit base is very different than your account value!

Let's dig into this annuity so you have a better understanding of the nuts and bolts…

Interest Crediting Options

It is important to understand that you are not investing in the underlying securities of any index. With index annuities, you are not making investment choices like a variable annuity. Your interest crediting options are mathematical formulas that the insurance company is using to attract you into buying xyz annuity. The insurance company invests your money in whatever they choose (likely diversified, conservative investments). They just have to earn a return higher than their mathematical formula (or interest crediting option) so they can pay you, their salesforce, marketing, operations, etc. This is why index annuities will likely only generate low single-digit returns.

For the Security Benefit Secure Income Annuity, you may select among three different interest crediting options: the Fixed Account, annual point-to-point index account with cap based on the S&P 500 Index and monthly sum index account based on the S&P 500 Index.

As of January 2014, the Fixed Account current interest rate was 1.50%. You should only choose this option if you believe the S&P 500 is about to have a terrible year. You don't want 1.5% returns every year because the GLWB rider will take most of that return leaving you with very little.

The S&P 500 option has an initial cap of 3.25% and a guaranteed minimum cap of 1%. As an example, the S&P had a stellar year in 2013 and was up 29.6% point to point. Because of the cap, you would be credited with a 3.25% gain for 2013. A far cry from true equity returns. Don't let any salesman lead you to believe that you can generate equity returns with this investment option. It is impossible. If you choose this option, your maximum possible return is 3.25% and your true return will likely be between 2-3%.

The monthly sum index cap is 1.6% with a guaranteed minimum cap of 1%. Salesmen may point out that 2013 was a banner year for the monthly sum option and this is undoubtedly true. However, this was an outlier and not the norm. Over a 10 year period, the monthly sum and point to point options will produce similar results to the point-to-point index.

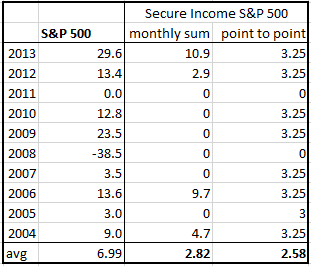

Here are the hypothetical results from the last 10 years. These are hypothetical because this annuity was only created in 2011. These are also assumptions based on current caps. Caps are subject to change at the end of each contract year.

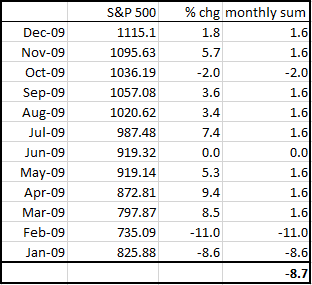

Note that either the monthly sum or point-to-point options resulted in similar returns for the 10-year period. They both trailed the S&P 500 by a wide margin. The monthly sum option had a great result in 2013, but it is hurt in volatile years like 2009 and 2010 where a few large down months wipe out all the gains of good months. Here is 2009 as an example for the monthly sum option.

In 2009, the S&P 500 was up over 23%. However, with the monthly sum option, you would have been credited with a big fat ZERO. As you are aware, your upside is capped out at 1.6% each month, however negative returns aren't capped. Therefore, the terrible months of January and February wipe out the capped returns of the rest of the year. This leaves you with no return for the year.

If you have additional questions about these options (I know they are tricky and complex), please submit a question using our secure form. We will answer your questions within 24 hours via email. No strings attached, just a little free help to point you in the right direction.

Who should buy this product?

In summary, the Security Benefit Secure Income is something to consider for someone that doesn't want to worry about market volatility, won't need access to their money for at least 10 years and wants a guaranteed income stream. This annuity will be most valuable for those people that are in great health and have a family history of longevity. If you can live into your mid-90s and beyond, you will surely do well with this annuity plus GLWB rider. Be sure to evaluate how it fits into your entire investment strategy and how it will help you reach your financial goals.

Just be wary of any agent that is promising too much in terms of returns. Remember that the 7% roll-up rate is not your rate of return. As shown above, your interest crediting options will likely return between 2-3% over the long term. Anything more than that is a pipe dream. Be especially wary of anyone who suggests this annuity will return 6% or more because it simply will not. An insurance agent once described index annuities to me as CDs on steroids. This is how you should think of them as well. They will likely perform slightly better than a CD but will never produce equity returns. Index annuities are designed to give peace of mind and protection from the downside. Just don't buy any sales pitch that is too good to be true.

Thanks for sticking with me on this incredibly long blog post. I learned a lot in my research process and I hope you are able to make a more informed investment decision because of it. Please don’t let your agent pressure you into a sale before you have made an informed decision. Since annuities lock you into a long-term contract with stiff surrender fees, please be sure to take your time to make the best possible decision for you and your family.

Have questions about this Annuity?

If you're considering this annuity and have additional questions, feel free to reach out. You can contact us via our secure contact form. We will answer your questions within 24 hours via email. No strings attached, just a little free help to point you in the right direction.

Have you purchased this annuity or are you doing your due diligence? Please share your experience in the comments section below.

“Annuities stock photo” by lendingmemo_com is licensed under CC BY 2.0