My weekends are packed with activities to entertain my 2-year-old daughter Chloe. Virtually all my friends have children, from newborns to kindergarten age. We all reminisce about the days when college was a third of the cost and wonder how the heck we will pay for our kids to go to college. With 50 colleges charging over $60,000 a year, where will prices be in another 10-15 years?!?!? My dad always thinks outside the box and he thought I should train to become a football placekicker so I could earn a scholarship. While definitely a cool idea, it never progressed past a Nerf football being kicked about 15 yards in the backyard.

Going the more traditional route today would be to invest in a 529 plan where the gains on investments are tax free when used for qualified educational expenses. Parents and grandparents should definitely take advantage of tax free growth! Last year I blogged about how to spend and save and my daughter's 529 is now over $3500 using that strategy.

In-state or Out-of-state 529 College Savings Plans?

When choosing a 529 plan, you should first check if your state offers a tax deduction for 529 contributions. Indiana is the most generous with a 20% tax credit on contributions up to 5,000 and Vermont gives a 10% tax credit per beneficiary. Please go to finaid.org to see what your state offers. So far 34 states and the District of Columbia offer some deduction on contributions. To take advantage of state tax deductions, you have to invest in a 529 plan in your home state so your investment choices are limited.

If your state doesn't offer any incentives or you don't pay state income tax, then you are free to purchase any 529 plan so you can be more selective. California, Delaware, Hawaii, Kentucky, Massachusetts, Minnesota, New Hampshire, New Jersey and Tennessee do not offer any incentives for college saving. While Alaska, Florida,, Nevada, South Dakota, Texas, Washington and Wyoming do not have state income tax.

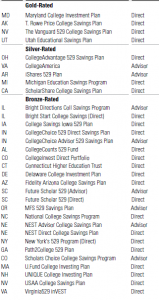

The Morningstar 529 Study: the Best and Worst of 2014

Morningstar recently released a special report on 84 of the top 529 plans. Each plan was ranked in 5 areas: Process, Performance, Price, Parent, and People. Each was then assigned to the Gold, Silver, Bronze, Neutral or Negative category. Here are the key takeaways from Morningstar's 50 page report.

Key takeaways:

- Assets in 529 plans grew 20% in 2013 to $200 billion, fueled in part by strong gains in stocks.

- Costs among 529 plans continue to decrease, although the investment options remain relatively pricey compared with most traditional open-end mutual funds. Dollar-based fees continue to eat away at returns for certain investors in roughly half of 529 plans.

- The annual Morningstar Analyst Ratings for 529 plans gave its highest Gold rating to four direct-sold plans. An additional 28 plans earned a Silver or Bronze rating, reflecting Morningstar’s view that they are expected to outperform on a risk-adjusted basis after tax benefits over a full market cycle.

Here are the cream of the crop from Morningtar's 2013 rankings:

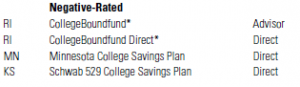

Here are the bottom of the barrel. If you are invested in these, you should consider rolling them into another plan because the fund fees are too high or there are other issues that Morningstar flagged in their 2013 rankings. Just this month, the Minnesota College Savings Plan cut their fees to less than 0.25% so I'd expect their rating to improve in the next rating report.

The bottom line

Being a resident of New Jersey, I don't get any tax deductions for contributions so I am free to choose among any 529 college savings plan. Last year I chose New York's 529 Program which offers a range of Vanguard investment choices and linked it to uPromise.com for my spend and save strategy. After seeing the Morningstar list, I worried that it is only a Bronze-rated plan so I looked into the Gold-rated Vanguard 529 Plan from Nevada. When comparing the plans, the Nevada Gold-rated plan has expense ratios of 0.21-0.50% and requires a minimum investment of $3,000. On the other hand, the NY Bronze-rated plan has a expense ratio of just 0.17% and requires a minimum investment of just $25. After comparing the plans, I decided to stay put with the NY 529 plan since both offer Vanguard investment options. In the end, you shouldn't blindly follow these rankings either. Make sure you do your own homework and make the decision that is best for your needs. Maybe I should get a Nerf football to start training Chloe…

By