In the short term, many factors can influence the direction of stock prices. We discussed central planners impacting the markets just last week. However over the long term, it's earnings that drive stock prices higher or lower. This is a simple concept to understand. If a company loses money year after year, it will struggle to stay in business. Not many people will choose to invest in a losing operation so the stock price will go down. On the other hand, if a company delivers consistent high levels of growth, it will attract many investors driving the stock price higher. This concept can also be applied to the broad market indices like the S&P 500. Therefore it makes sense to look at S&P 500 earnings estimates.

The Good: Healthcare, Technology and Consumer Discretionary

No matter what the situation is, there are always good opportunities to be found. When looking at the individual S&P sectors, healthcare, technology and consumer discretionary are still pointing to strong growth in 2015. All three of these sectors are showing double-digit growth. Year to date, these sectors have also seen stock prices appreciate. Healthcare (XLV) is up 6%, Consumer Discretionary (XLY) is up 4.8% and Technology (XLK) is up 4.5. Hopefully estimates will also see upgrades from gas savings, cheaper imports, cheaper manufacturing and lower transportation costs.

The Bad: Shrinking expectations

On November 26, 2014, S&P 500 earnings estimates pointed to a robust $133.38 or 14% growth for the broad market in 2015. This number was surprising healthy given that oil prices declined so sharply since the summer. However it turned out that analysts were behind the curve and reduced estimates sharply in just two months. Today street estimates for the S&P 500 have been reduced to $118.32 or 5% growth for 2015. The energy sector had the largest impact in the reduction in S&P 500 estimates; however estimates in every sector decreased over the last two months. This can be attributed to the strong Dollar negatively impacting international earnings and slowing global demand.

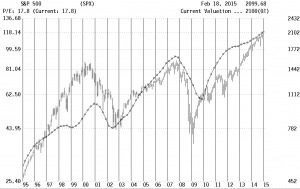

The Ugly: Earnings contraction

Using rolling 4 quarter estimates, we see flat growth for the 2nd and 3rd quarters but companies tend to be conservative in their estimates early in the year. This picture should become clearer after first quarter earnings are reported and companies have a better feel for how the year is taking shape. For now, the ugly hasn't arrived and isn't in sight. As seen in the chart above, you don't want to own the S&P when earnings contract like the periods of 2001 and 2008. This bears close watching as earnings are weakening but not turning over.

By